Funding-Rate Harvest (Round 1)

Delta-neutral cash-and-carry funding harvest

The program's first mechanical (not structural) failure. The funding premium is real and wildly significant — placebo 95th percentile 0.003, ~13%/yr gross. The literal rebalance rule fails 4/8 gates on whipsaw transaction-cost drag. A re-pre-registered hold-continuous rule is now in a fresh paper window.

- Category

- Carry (crypto)

- Window

- Locked OOS 2024-04 → 2026-06 (115 weekly obs)

- Instruments

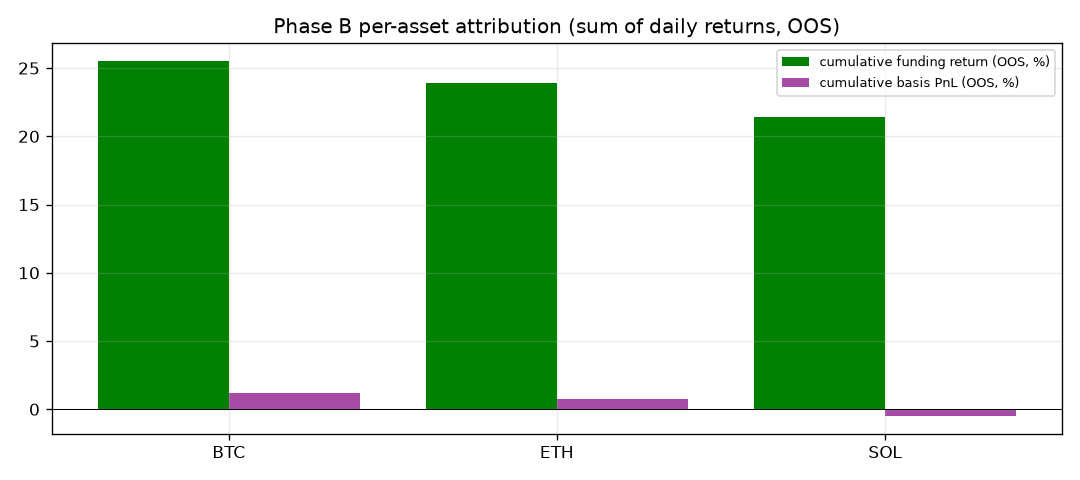

- BTC, ETH, SOL (spot long + perp short)

- Timeframe

- Daily rebalance, weekly evaluation

- Tested

- 2026-06-21

The first failure that wasn’t a no-edge

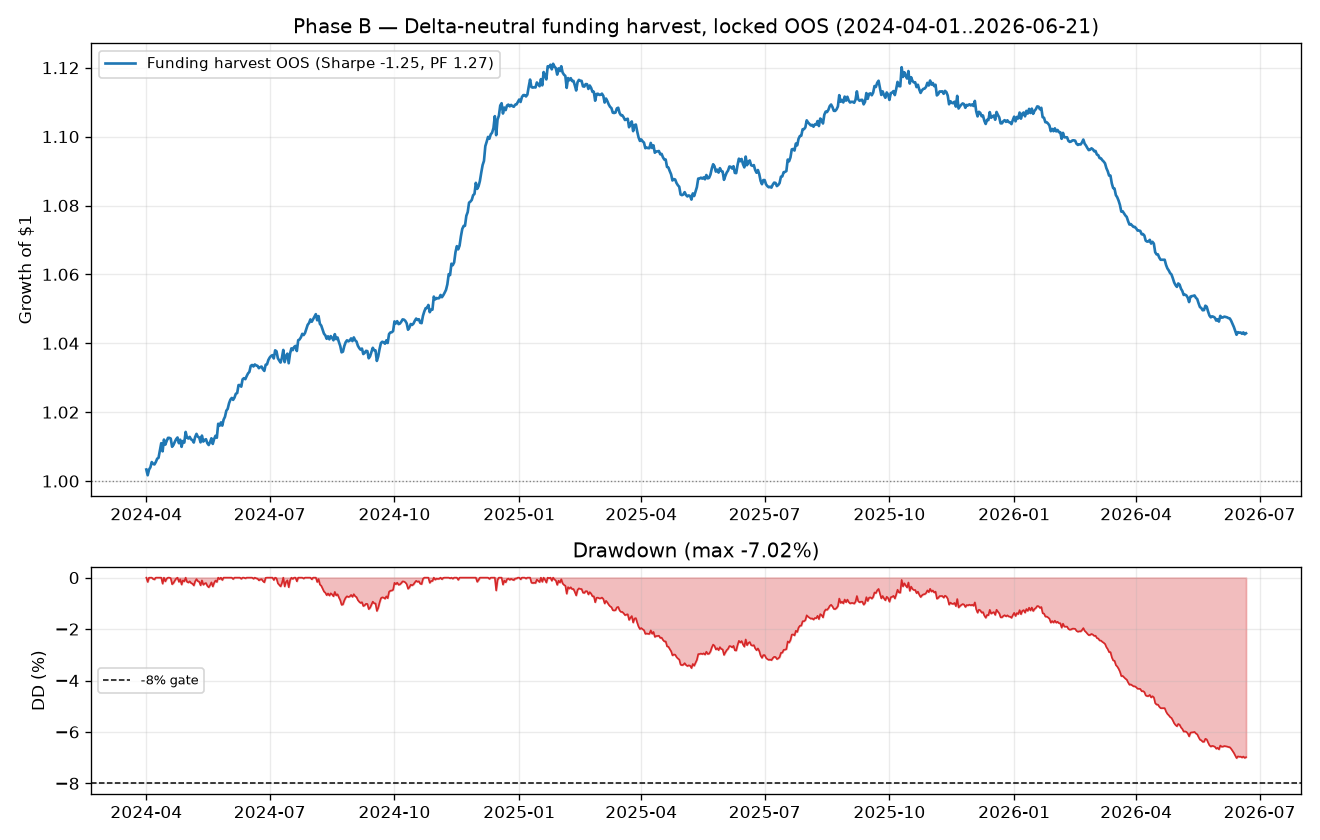

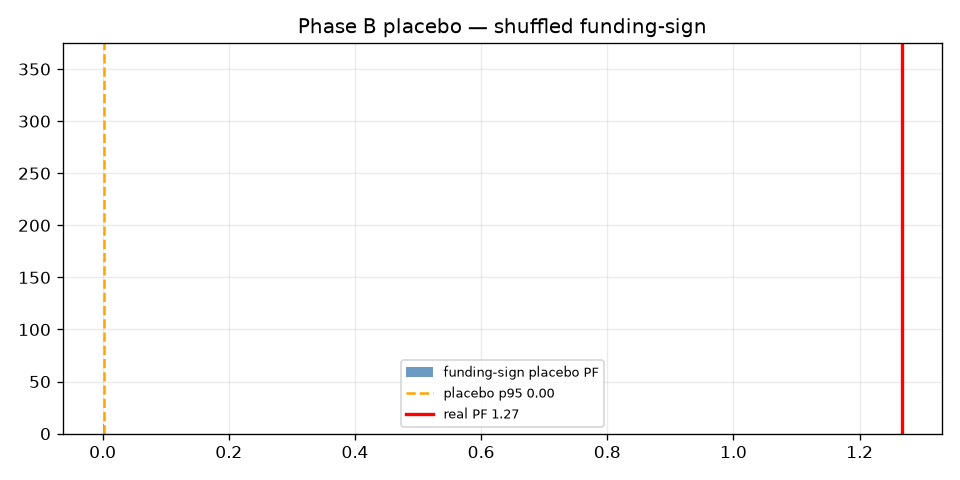

For the first time in the program, a strategy failed its gates without failing for lack of an edge. The delta-neutral funding harvest — long spot (BTC/ETH/SOL), short the Hyperliquid perp, collect funding while staying market-neutral — sits on a premium that is real and statistically overwhelming. Funding is positive 75–87% of hours, averaging +13–15%/yr gross, and the placebo is decisive: real PF 1.267 vs the random-permutation 95th percentile of 0.003, with 0% of 500 shuffles matching it.

And yet, run on its pre-registered literal rule over the locked out-of-sample window, it fails 4 of 8 gates.

Gate scorecard — 4 / 8 (literal rule)

| Gate | Threshold | Result | Pass |

|---|---|---|---|

| G1 weekly OOS obs | ≥ 60 | 115 | ✅ |

| G2 PF net of costs | ≥ 1.20 | 1.267 | ✅ |

| G3 Annualized Sharpe | ≥ 0.6 | −1.25 | ❌ |

| G4 Max DD | ≤ 8% | −7.0% | ✅ |

| G5 Block-bootstrap LB Sharpe | > 0 | −1.54 | ❌ |

| G6 Placebo: real PF > p95 | beat | 1.267 vs 0.003 | ✅ |

| G7 DSR / PSR(SR>0) | > 0.95 | 0.847 | ❌ |

| G8 2× cost stress PF | > 1.0 | 0.494 | ❌ |

Mechanical, not structural

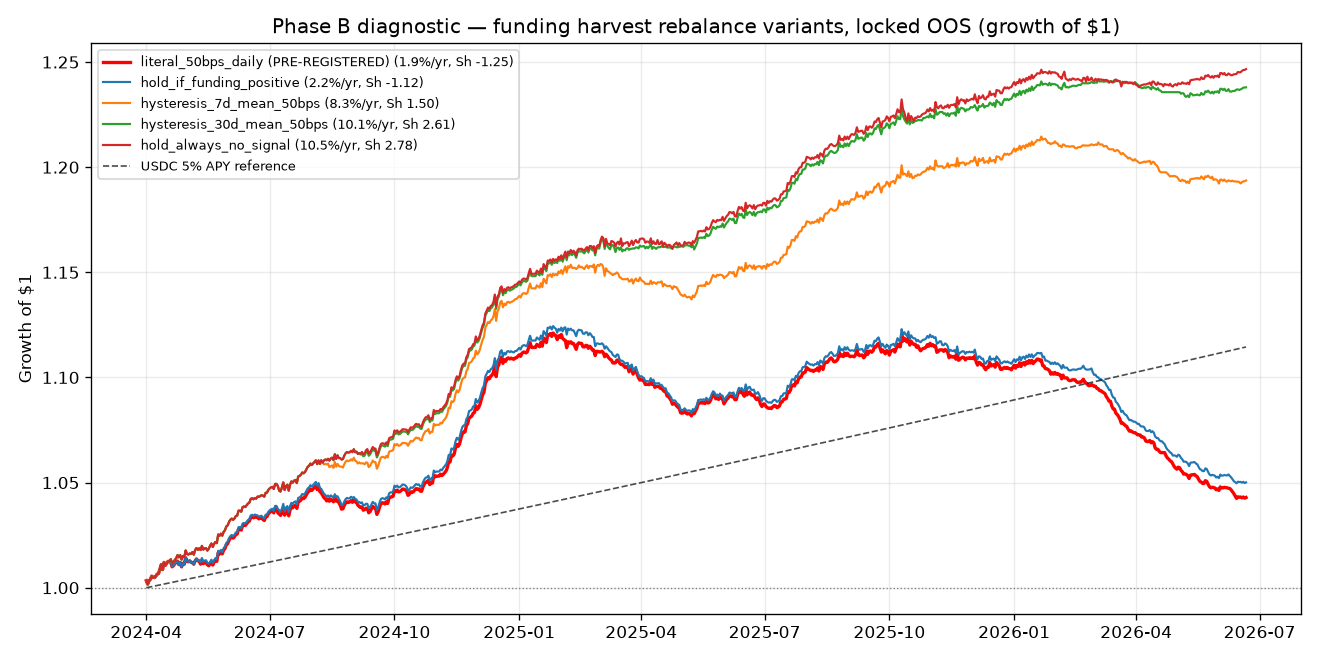

The placebo result is the tell — the edge is not the problem. The strategy fails on whipsaw transaction-cost drag. The pre-registered 50-bps threshold sits ~25× below the ~1,300-bps mean funding, so it never gates entries; it only triggers exits every time daily funding briefly dips, then re-enters the next day:

| Coin | Transitions/yr | % time in position |

|---|---|---|

| BTC | 36.4 | 89.7% |

| ETH | 58.9 | 84.5% |

| SOL | 61.6 | 72.9% |

At ~0.26% per round-trip, 36–62 round trips/yr burns ~8–9%/yr — turning a +13% gross premium into +1.9% net, below the 5% USDC risk-free. A diagnostic shows the same hypothesis held without churn (30-day-mean hysteresis) would clear all eight gates with Sharpe 2.6 and sub-1% drawdown — but reading that off the same window would be exactly the data-snooping the program forbids. This OOS window is now burned for the corrected rule.

Why it’s in the paper window, not retired

This is the disciplined disposition the framework is built for: a genuine, placebo-confirmed premium underneath a mis-specified execution rule earns “proceed to Round 2,” not “retired.” The corrected hold-continuous / hysteresis rule is being evaluated on a fresh, untouched window (forward-only or 60+ days of live paper trading) before any capital. Indicative Round-2 expectation: ~8–10%/yr net at ~2% vol — a cash-plus, low-risk Sharpe play, not a moonshot.

Verdict: PAPER (Round 1 failed, edge confirmed). The funding premium is real and statistically overwhelming; the pre-registered rule churns it away on costs. A re-pre-registered hysteresis rule is in a fresh paper window — capital waits for a clean pass.

Charts & evidence

Frequently asked

Is the crypto funding-rate harvest a real edge?

Yes — the underlying premium is real and statistically overwhelming. In the delta-neutral cash-and-carry setup (long spot, short perp), funding is positive 75–87% of hours and averages +13–15%/yr annualized across BTC, ETH and SOL. The placebo test is decisive: the real profit factor of 1.267 beats the random-permutation 95th percentile of 0.003, with 0% of 500 sign-shuffled placebos matching it. This is the first edge in the program that is not a structural no-edge result.

Why did the funding harvest fail its gates if the edge is real?

Whipsaw transaction-cost drag — a mechanical, not structural, failure. The pre-registered 50-bps threshold sits about 25× below the ~1,300-bps mean funding, so it never gates entries; it only triggers exits every time daily funding briefly dips, then re-entry the next day. At 36–62 round trips per year and ~0.26% per round-trip, that churn burns ~8–9%/yr, converting a +13% gross premium into +1.9% net — below the 5% USDC risk-free rate, hence the negative Sharpe despite PF > 1.

What happens next with the funding harvest?

A Round-2 re-pre-registration. A diagnostic shows the identical economic hypothesis expressed without churn — a hysteresis rule on 30-day-mean funding — would clear all eight gates with large margin (Sharpe 2.6, drawdown <1%, cost-robust to 2×). But swapping the rule and re-reading the same window would be data-snooping, so the 2024-04→2026-06 window is now burned. The corrected rule must be evaluated on a fresh, untouched window or via 60+ days of live paper trading before any capital.

Methodology: The Validation Gauntlet — pre-registered spec, 8-gate battery, real market data.

Full reproducible report: research/hyperliquid_funding/REPORT.md in the source repository.

Author: Brent Akamine (Founder, Vinovest). Backtests are not investment advice.