Pairs Trading ETH/BTC (Cointegration)

Cointegration mean-reversion statistical arbitrage

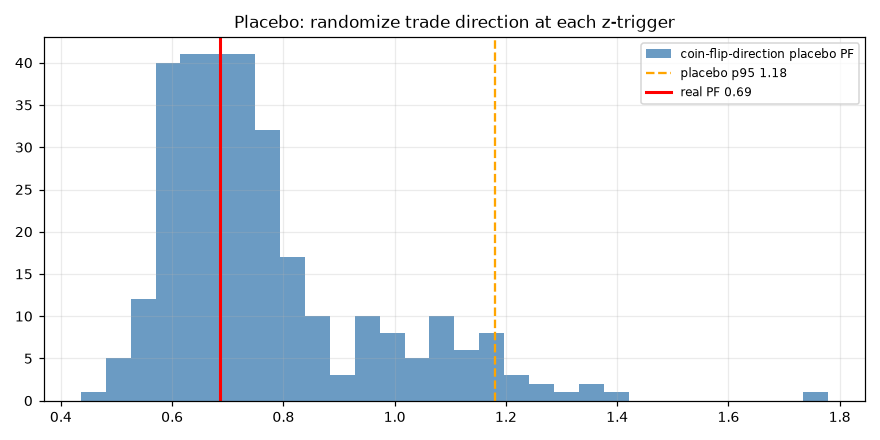

Placebo failed — 58% of random-sign permutations beat the real strategy. Only 46 trades in eight years, a −93% drawdown driven by the 2021 regime break, and in-sample PF 0.49 versus out-of-sample 1.34. The ETH/BTC cointegration relationship did not persist tradeably.

- Category

- Statistical arbitrage

- Window

- 2018–2026 (ETH vs BTC)

- Instruments

- ETH/BTC (crypto)

- Timeframe

- Daily, z-score spread

- Tested

- 2026-06-25

The story in one line

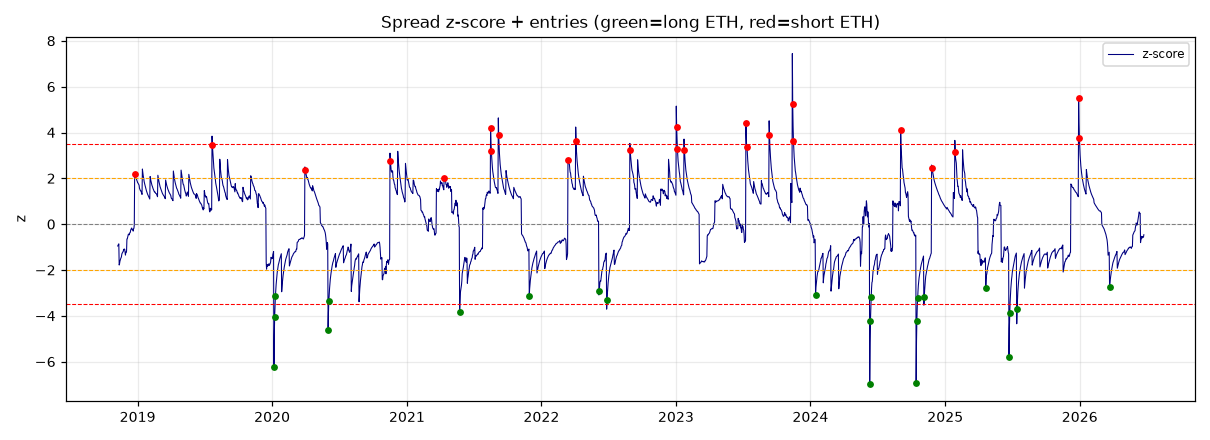

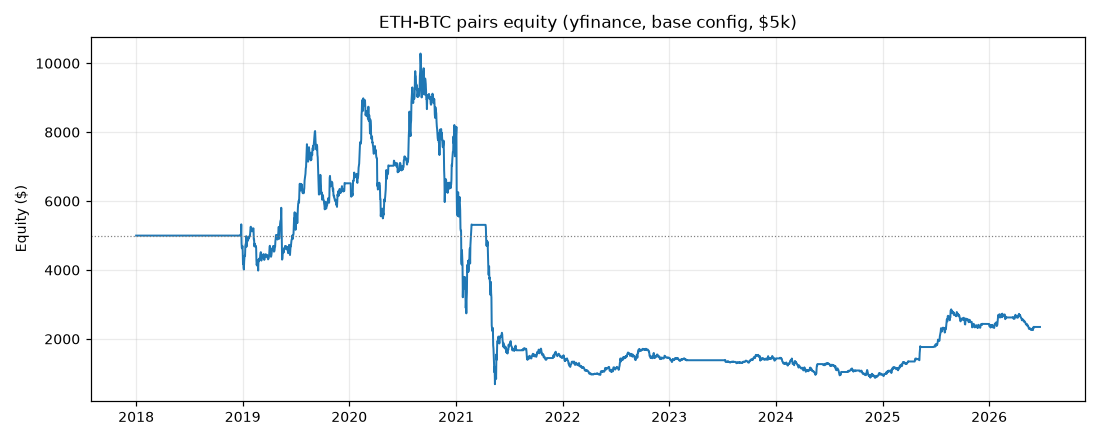

A textbook cointegration pairs trade on ETH/BTC — z-score the spread, fade it at ±2σ, exit at 0, stop at ±3.5σ — over 2018–2026 finishes at $2,349 from a $5,000 start (net −$2,651), profit factor 0.686, Sharpe 0.10, max drawdown −93.3%, on just 46 trades in eight years with a 50% win rate. It passes 2 of 11 gates, and both are technicalities (a positive deflated Sharpe driven by a near-zero raw Sharpe, and a walk-forward check the strategy “passes” only because in-sample is so bad that out-of-sample clears 0.9× of nothing). The decisive failure is the placebo: 58.3% of random-sign permutations beat the real strategy (real PF 0.686 versus placebo p95 of 1.181). The ETH/BTC relationship did not persist tradeably.

What the cointegration test showed

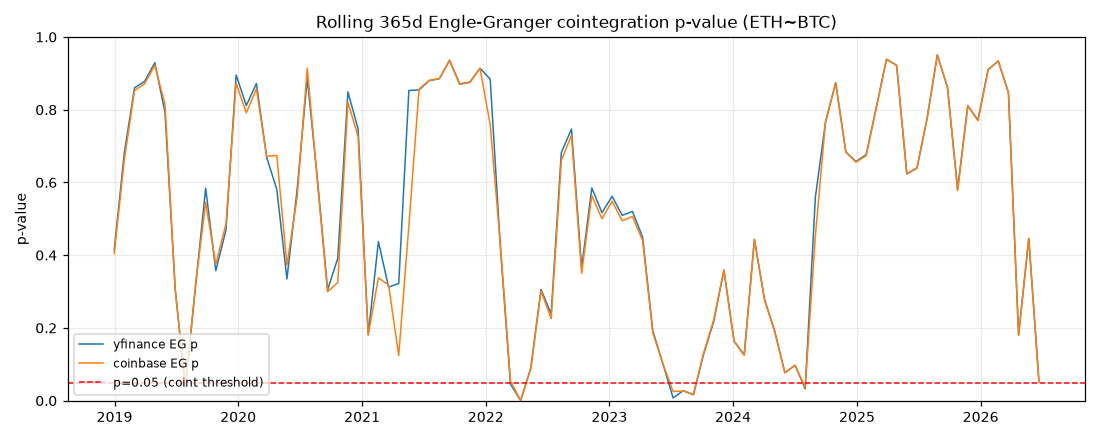

The pair never cleared a cointegration bar to begin with. Engle–Granger gives p = 0.322 (ETH on BTC) and p = 0.654 (BTC on ETH) — both far above 0.05 — and the residual ADF p-value is 0.139, so the spread is not stationary at any conventional level. The Johansen trace statistics (7.65 and 1.45) sit below their 95% critical values (15.49, 3.84), confirming no cointegrating vector. The estimated hedge ratio (β ≈ 1.05) is sensible, but the spread’s half-life of mean reversion is ~486 days — far too slow for a tradeable signal and longer than most of the holding windows the strategy actually used. Worst of all, the rolling cointegration fraction is just 7.6%: the relationship was cointegrated in only about one window in thirteen across the sample.

Why it fails

The signal underperforms random. In 300 sign-flipped permutations, 58.3% beat the real strategy and the placebo 95th percentile (1.181) sits well above the real PF (0.686). Whatever P&L exists is not attributable to the cointegration signal.

It barely trades. 46 trades in eight years — under six a year — fails the 100-trade minimum and means every result rests on a handful of events. There is no statistical mass here.

In-sample and out-of-sample disagree completely. IS PF 0.486 versus OOS PF 1.336. A real edge is stable across the split; this one inverts. The “passing” walk-forward gate is an artifact of how broken the in-sample half is, not evidence of robustness.

One year ate the account. The 2021 regime break dominates everything: −$6,116 in 2021 against gains of roughly +$1,517 (2019), +$1,046 (2020), and +$1,446 (2025). ETH structurally repriced against BTC and the mean-reversion bet — that the spread snaps back to its historical band — kept fading a move that did not revert, producing the −93.3% drawdown and a single-year P&L share of 56%.

Verdict: REJECTED (PF 0.686). Do not deploy. The pair is not cointegrated (EG p 0.32, ADF p 0.14, rolling coint 7.6%), the half-life (~486 days) is untradeable, and a random sign-flip beats the strategy 58% of the time. The ETH/BTC cointegration relationship did not persist tradeably over 2018–2026.

Charts & evidence

Frequently asked

Does ETH/BTC cointegration pairs trading work?

Not tradeably over 2018–2026. A z-score cointegration pairs strategy on ETH/BTC returned a profit factor of 0.686 with a −93% drawdown, and it failed the placebo test — 58% of random-sign permutations beat the real strategy. The relationship also broke between in-sample (PF 0.49) and out-of-sample (PF 1.34) windows, and the system took only 46 trades in eight years.

Why did the ETH/BTC pairs strategy have a 93% drawdown?

The 2021 regime break. ETH structurally repriced against BTC during 2021, and a mean-reversion spread trade that assumes the ratio returns to its historical band took a −$6,116 hit that year — the dominant loss in the whole backtest. Cointegration measured on history is not a guarantee the spread stays stationary, and here it did not.

Methodology: The Validation Gauntlet — pre-registered spec, 11-gate battery, real market data.

Full reproducible report: backtests/pairs_ethbtc/results.json in the source repository.

Author: Brent Akamine (Founder, Vinovest). Backtests are not investment advice.